Numerous pharmacy closures have been predicted ever since the opening of the first Chemist Warehouse in October 2017 and the introduction of the evergreen Integrated Community Pharmacy Services Agreement the following year.

Three years on, more pharmacies are closing but that number is eclipsed by new businesses opening, despite widespread concerns about the financial sustainability of the sector.

Figures from the Ministry of Health show that from July 2018 to now, 69 pharmacies have closed across the country, while 97 new pharmacies have opened.

The rate of closures does seem to have stepped up in the past two years. Between July and December 2018, just five pharmacies closed nationwide. Thirty-one pharmacies closed in both 2019 and 2020 but in both years more opened, 37 in 2019 and 33 in 2020.

So far in 2021, two pharmacies have closed and two have opened.

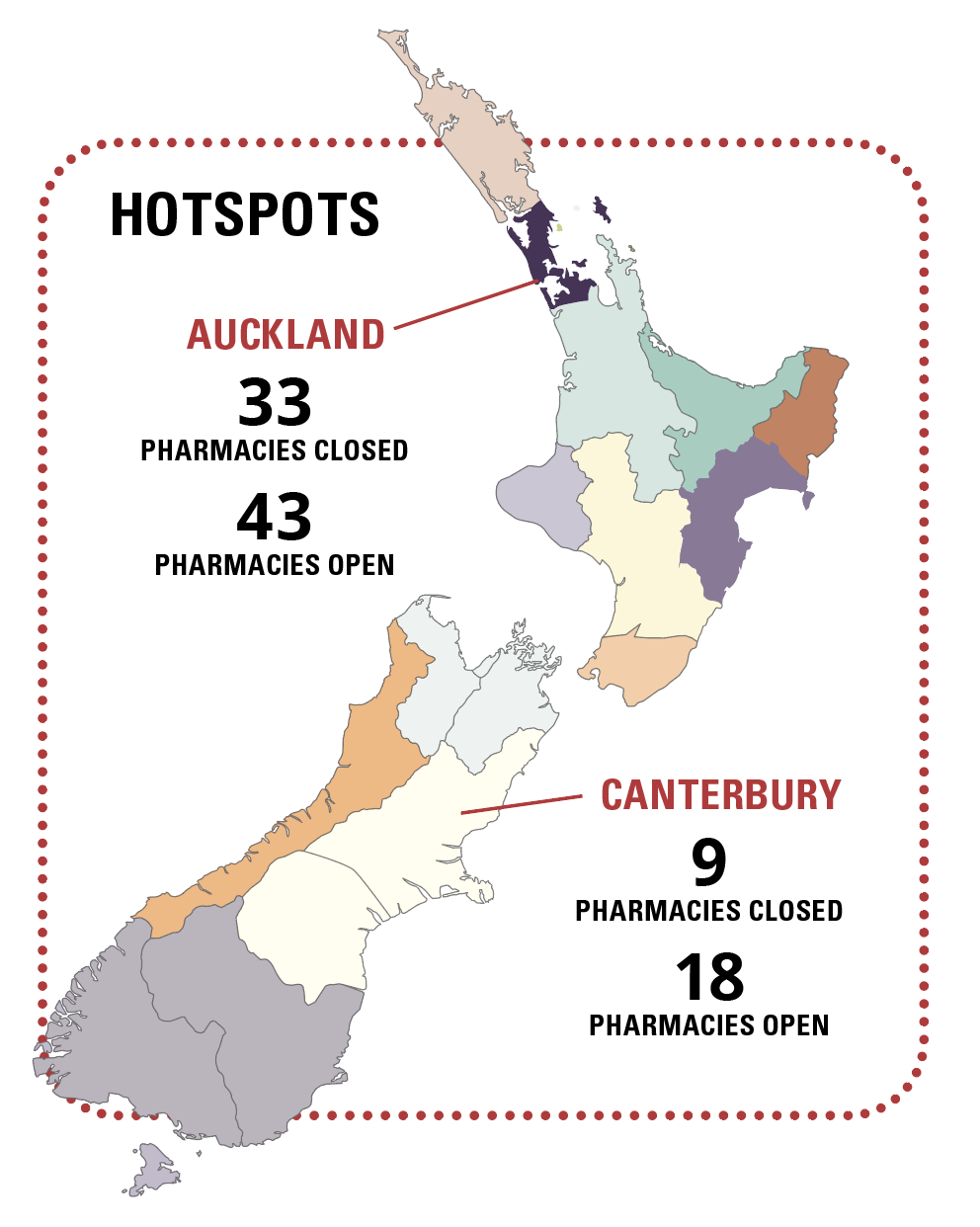

Broken down by DHB regions, it is clear most of the action is happening in Auckland and Canterbury, the areas most affected by competition from discounters. In Canterbury, nine pharmacies closed and 18 opened during this period. And in Auckland, 33 closed and 43 opened.

69 pharmacies closed since July 2018

The Auckland district was the only large DHB area where the number of pharmacies that closed was slightly more than the number that opened in both 2019 and 2020.

Jonathan Roberts, Auckland director at the accountancy firm Moore Markhams, says most of the new pharmacies he is aware of opening now are large ones, either discounters such as Chemist Warehouse and Countdown, or other large corporates, often at purpose-built medical centre sites.

This observation is true for the Ormiston Kiwi Chemist, a new 100sqm pharmacy that opened last month in a brand-new, purpose-built 3000sqm medical centre in the Auckland suburb of Flatbush.

Owner Michael Mishriki believes selecting a good location is key to running a successful pharmacy in the current climate.

“You just have to be a bit more discerning with the pharmacies you open or buy.”

For instance, the medical hub housing his pharmacy includes six doctors, a dentist, a physio and a radiologist so it should have a good volume of prescriptions in addition to its retail.

The pharmacy is Mr Mishriki’s fifth, and he is not discounting prescription fees in an attempt to compete with discounters at any of them.

He believes independents can still compete, if they do everything they can to look after their patient base.